From the Goods and Services Tax (GST) perspective, renting residential and commercial property is treated as a ‘supply of service’. The GST on rental income will be levied only if the annual rent is above Rs 20 lakh and that too at an 18 percent rate.

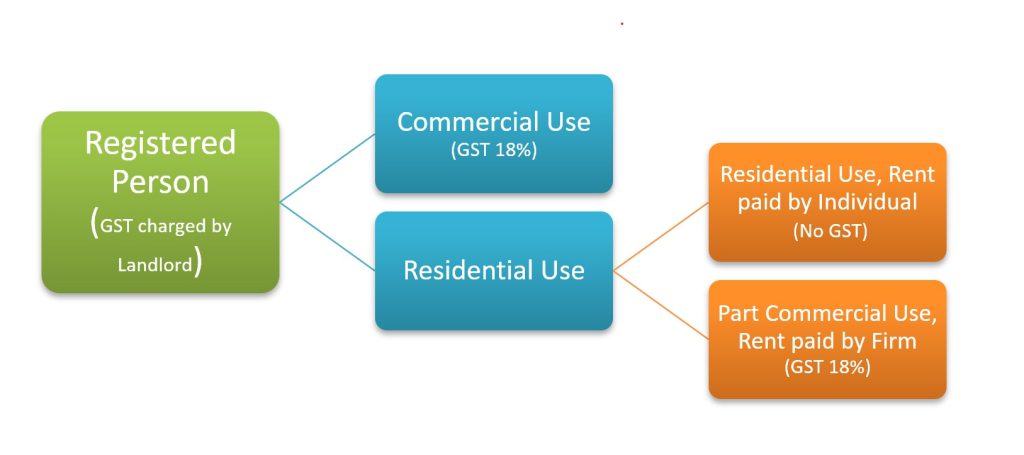

Under the residential dwelling, if the landlord is registered under GST, then the GST is charged only if the property is leased for commercial purposes or part of the property is leased for commercial purposes. If the property which is leased for residential purpose only or part of property is leased for residential purposes then no GST is implied.

GST on Rental Income, Registered Person

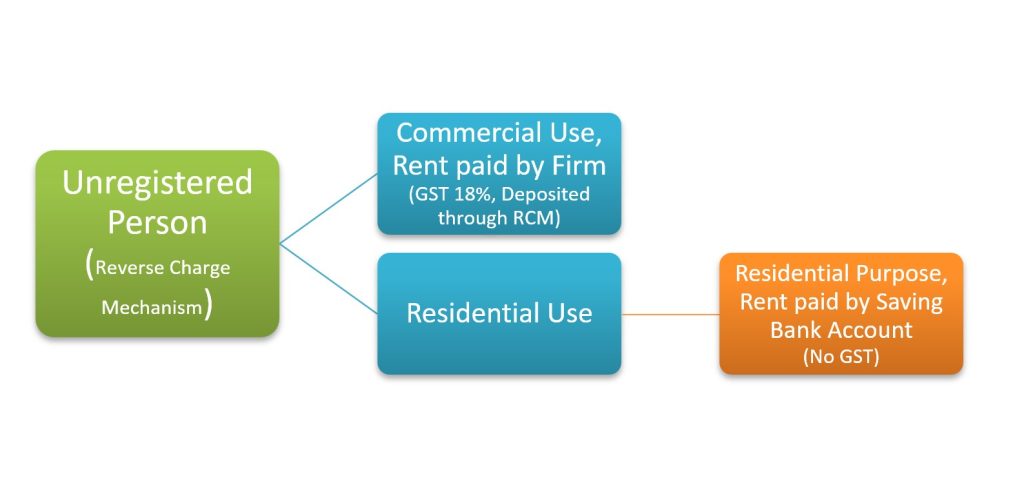

Alternatively, if the landlord is not registered under GST, then Reverse Charge Mechanism (RCM) is implied. Under this, if a property is used, in full or part, for commercial purposes then the lessee has to deposit the GST under RCM. Also, if the rent is paid through the Firm, then GST has to be deposited by the lessee under RCM. The property is completely free from GST as the use is only residential.

From the Goods and Services Tax (GST) perspective, renting of residential and commercial property is treated as a ‘supply of service’. The GST on rental income will be levied only if the annual rent is above Rs 20 lakh and that too at 18 per cent rate.

Under the residential dwelling, if the landlord is a registered under GST, then the GST is charged only if the property is leased for commercial purpose or part of the property is leased for commercial purpose. The property which is leased for residential purpose only or part of property is leased for residential purpose then no GST is implied.

GST on Rental Income, Registered Person

Alternatively, if the landlord is not registered under GST, then Reverse Charge Mechanism (RCM) is implied. Under this if property is used, in full or part, for commercial purpose then the lessee has to deposit the GST under RCM. Also, if the rent is paid through Firm, then GST has to be deposited by the lessee under RCM. The property is completely free from GST as the use is only residential.